#1.1 Feasibility & Timeline

For majority of the people around the world, house is “constructed once in lifespan” and hence “first time right” is the only option.

If you plan to construct house then Its always good to get guidance from experienced person. We will ensure that you are better equipped with the knowledge to self-analyze the use cases based on the pros & corns provided to fullest depth. Reviews shared will be based on consumer evaluation of the products over years of use. The information provided will be from the experienced industrial expert in the construction domain.

So pin this page and like the channel for a single point of reference for complete construction solution.

- Should you buy a house / Land / Rent ?

- When to purchase self occupied property

- When to go for EMI option / Finance criteria for purchasing House.

#1.1.1 Should you buy a house / Land / Rent ?

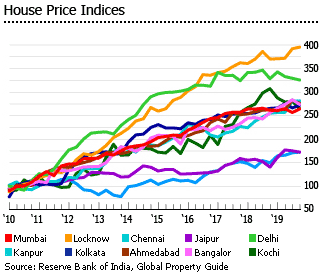

Rent and Land purchase cost go nearly hand in hand. As per all-India HPI increased (y-o-y) by (+)2.7 per cent in Q4:2020-21 vis-a-vis (+)3.9 per cent growth a year ago; HPI growth showed large variation across major cities, from an increase of (+)15.7 per cent (Bengaluru) to a contraction of (-)3.6 per cent (Jaipur).

(Source : RBI Press Release: 2021-2022/403)

If your disposable income is grater then of 5 times or more then monthly rent amount but you do not know where to invest. Its obvious that spending hobbits and lifestyle will start utilizing this surplus amount. The below article will help you put your surplus to passively work for you.

Note: Ensure the you read the Pros and Corns section to make a wise choose that suites your need.

#1.1.2 Why to purchase a house (Pros)

- Below are some of the catalyst that makes purchasing / owning a house sensible but ensure you read the Corns, Finance and EMI part before going for any of the option below.

- Refer : Land purchase for more detail.

Investing in real estates is one of the secure investment if done rightly. Land is real asset unlike stocks , bonds, Fixed Deposit (FD) or fiat currency stored in bank. This is only true in a growing economy where the population is booming. Negative growths are seen in countries like japan, Greece and now in China where the population is on the decline and so are the housing markets.

- it’s the Land that appreciate in value not the constructed house/building. Hence owning large empty land spread over different geographical location is a wise choice in case of return on investment.

- Land can appreciate in value as low as 1-5% YOY in developed residential cities , 5-15% YOY in developing cities, -10% to +50% or more YOY in suburban areas base on potential of development by both government and private bodies.

- Government projects like metro train, parks , Hospital, economic corridors / hubs

- Private Projects like shopping Mall , IT park, apartments

- For a constructed house the value of appreciation is 1-3% on average as the structure weeks over time life time is consider 30-50 Years for a concrete roof structure.

Exceptional case is commercial buildings where value appreciation is 5-10 % even if the building is constructed and is old. This is true for in case situate in high economic zone thus fetching more in revenue for the business operating there.

Example : Im sure we all have also seen space beneath buildings near the staircase being used for printing shops or small commercial businesses

10 feet by 5 feet can be used to rent ATM machine space to bank.

- House is not just for self but for the next generation to come. If you have already lived in a rented house in a specific part of city/town + you like the local vibes + would like to live there for long term, retire with old friends, relative or old neighbors, then its good to purchase the house in that locality. Example : I like Bangalore as I have been in this city for a very long time over 25Years. My family has lot of friends, relatives in north Bengaluru and have adjusted to the place. I used the below facility Vs Stakeholders table to evaluate and make a choice to construct house in North Bangalore.

Facility \ stakeholders requirement | Self | Parents | Children | Average score | City Offers Comments |

Medical facility | 3 | 4 | 3 | 3.3

| World class |

Educational intuition | 3 | 1 | 4 | 2.7

| IISC,IIM, Top ranking Institution. |

job market | 4 | 2 | 4 | 3.3

| Good |

Grocery / essentials | 4 | 4 | 4 | 4

| Home delivery , super market, hyper market |

entertainment | 2 | 2 | 3 | 2.4

| World class, 3D, 4D. |

Connectivity infrastructure | 4 | 4 | 4 | 4

| Traffic issue, Water crises predictions.

|

Cost of living | 4 | 3 | 3 | 3.3 | Medium – Very High |

If you are an employ who has a fixed job location, fixed wages and promotions. then based on lifestyle and financial checks mentioned in the article you can go ahead with purchase. make sure you read the corns section in case of unconsidered factors.

- Insufficient Saving habit : Not many millennials and Gen Z are as conservative as previous generations. Its natural to get the urge to purchase a new set of expensive watch , iPhone via Credit card, new bike or car via personal loan specially when there is an really good offer. But the question is …. “Do I really need it ? ” that get ignored. By restricting your financial income by availing home loan you are investing on a real long term asset.

NOTE:- EMI is subjected to RBI repo rates changes.

- This is a rigid & risky financial strategy and hence a backup and emergency savings plan is a must.

- House has low liquidity asset

- Appreciation value is subjected to market conditions, government influence and neighborhood.

- Read #1.1.3 Why Not to purchase a house (Corns) before considering these options.

- If your immediate family (you, parents ,children) do not own a house yet not even in village then its worth purchasing

- If you are undivided family (immediate family + sibling’s Immediate family) who want to build a house for permanent stay for generations. Then each member can contribute and divide the floors / rooms. This option is subjected to family cooperation better have a written agreement with the stake holders.

In country like Bharat, parents prefer a well settle groom with individual house or land. Most parents gaze on property portion rather then any other form of investment portfolio. If you happen to end up in similar situation or be prepared for such scenario then this option is for you.

Note : Only consider this option if you feel economically stable and have read all the Pros and Corns in article.

#1.1.3 Why Not to purchase a house (Corn)

- Mortgage is immovable asset : Once the investment is done its difficult to relocate. certainly you can sell and liquidate the amount but it takes time and is a lot of work to move. If you are planning to move around cities and your disposable income allows you to afford only one own house in you lifetime, then you must think twice unless you have an alternative plan before jumping into immovable asset like a house

- Restricted Career locations : If you are a person who has just started career, its eminent you are trying to explore your options until it complements your passion. Thus resulting you to switch and relocate. Even if you are a decade year experienced individual in case of changing lifestyle, family reason , etc it highly likely you would have to upgrade job to a new city or new country.

- Restricted Job upgrade/ transfer : Unlike japan where an employee spends his/her entire life in single company , in India and IT professional seem to switch 5 jobs on average over 30 years of working life. same goes government employee who get transferred frequently and then purchasing one large house in hometown for parents, sibling and family makes much more sense.

- Insufficient Saving habit : Not many millennials and Gen Z are as conservative as previous generations.

- Lack of Financial literacy

- Early investment also restricts you to explore jobs opportunity, explore better investment options, explore new places to visit and see a broader world.

If you are financial literate and have a good surplus saving then investing in a real-state could create a drag on you RIO (return on investment). rater you can invest in a high risk high return, business, etc, exit at right time and use the returns to purchase a real-state. as your risk taking capability in 20s is high and 30s is moderate. you will have parents and friends to back you up in case you encounter financial loss.

If you do not have a plans to make best use of only feasible property by renting portion of your building floor either residential, office space or something else. Then the house might not really be considered an asset rather it become a liability that takes money out of our pocket. Yearly average maintenance of 10K-20K loss.

In this case rather to invest in other asset class like Mutual investment or business. Most financial expert would recommend to stay in rented house or even better lease and spend your life happily with no financial worries.

#1.1.4 When to go for EMI option / Finance criteria for purchasing House.

- Disposable income shall be grater then of 5 times or more then monthly rent amount

- if you stay in rented house, this is the most important and fundamental calculation. The rent and house cost of the city is variable base on the area / city you stay. Commonly its noticed that for a construction of new house the total EMI costs minimum of 5 to10 times the monthly rent amount as to that of the same exact house dimension of rent.

- Example if you pay is 10,00Rs/Month in rent, 30K on essentials amenities and save 50K / Month. This would be a good option.

- Risk :

- In above example one must consider the yearly increment to be min of 10% YOY to compensate the inflation on essentials amenities

- EMI are subjected to change in case of RIO change by Government (refer : Home Loan section for more detail)

- Medical emergency and other essential concerns are secured and anchored

- Ensure you have term insurance in case of protecting family for unfortunate event

- if you stay in rented house, this is the most important and fundamental calculation. The rent and house cost of the city is variable base on the area / city you stay. Commonly its noticed that for a construction of new house the total EMI costs minimum of 5 to10 times the monthly rent amount as to that of the same exact house dimension of rent.